Bitcoin’s Valuation Outruns Onchain Growth – What’s Driving It

Bitcoin’s market value is rising faster than visible network adoption, shifting attention toward corporate demand, AI-driven portfolio rotation and a macro backdrop shaped by cooler inflation and persistent fiscal deficits.

Key Takeaways

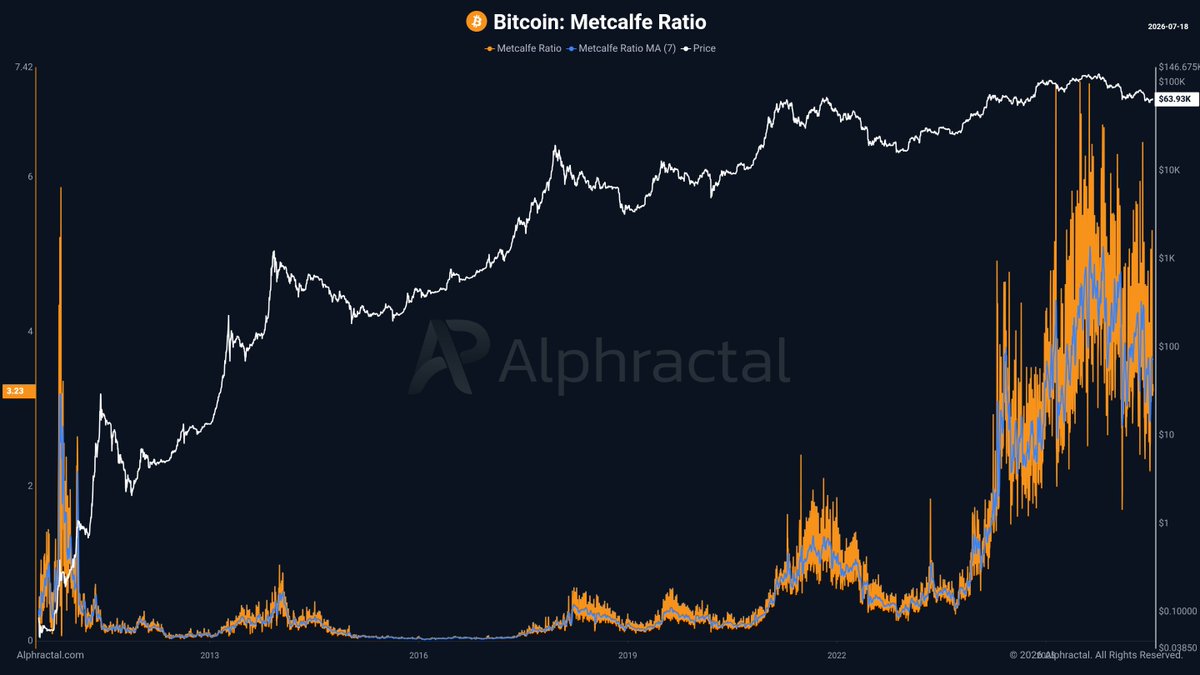

- Bitcoin’s Metcalfe Ratio near 3.23 suggests its valuation is rising faster than the network activity measured by the model.

- Corporate and institutional purchases can bring substantial capital into Bitcoin without producing an equal increase in active addresses or transactions.

- Michael Saylor sees corporate adoption as necessary for Bitcoin to develop into a global monetary network.

- Jordi Visser argues that Bitcoin is less exposed than traditional companies to competitive disruption from artificial intelligence.

- Cooler inflation and persistent U.S. fiscal deficits strengthen the macro case, but durable demand still needs to justify the valuation gap.

Bitcoin’s Valuation Is Moving Faster Than Its Network

João Wedson, founder and CEO of Alphractal, summarized the signal directly: Bitcoin’s valuation is outpacing network adoption.

The Metcalfe Ratio attempts to compare Bitcoin’s market value with activity across its network. A reading near 3.23 does not provide a precise estimate of fair value, but it indicates that market capitalization has increased more quickly than the adoption measure underlying the model.

Alphractal’s official API documentation lists the Metcalfe Ratio among its Bitcoin market indicators, alongside separate measures for network maturity, adoption and valuation.

The ratio remains a model-specific signal rather than a universally accepted measure of Bitcoin’s fair value. Its interpretation depends on the network inputs, historical relationships and methodology used to construct it.

That distinction matters. A rising price accompanied by equally strong network growth suggests that economic activity is expanding alongside valuation. When price moves much faster, the market is paying in advance for adoption that has not yet appeared in the same proportion.

The strongest conclusion is therefore narrower than declaring Bitcoin overvalued. The chart shows that the demand supporting the current market capitalization is not being matched by the same rate of growth in the onchain activity measured by Alphractal’s model.

Corporate Demand May Not Appear in Onchain Adoption

Onchain activity and economic adoption are no longer interchangeable.

A new self-custody user may create an address and generate transactions that appear directly in network data. A company, exchange-traded product or institutional investor can acquire a much larger position through a custodian while producing relatively little identifiable activity on Bitcoin’s base layer.

The same compression occurs when thousands of investors gain exposure through one investment vehicle. Their capital remains economically relevant to Bitcoin, but it may be represented onchain by only a small number of consolidated wallets and transactions.

Michael Saylor’s corporate-adoption argument connects with the Alphractal signal.

Saylor argues that companies allow people and capital to organize under a legal structure with greater scale, continuity, transparency and access to credit. For Bitcoin to succeed as a global monetary network, he wrote, corporate adoption is “necessary, inevitable, and welcome.”

Companies enable people to organize under law around a shared mission with greater efficiency, transparency, creditworthiness, scale, resilience, and continuity.

For Bitcoin to succeed as a global monetary network, corporate adoption is necessary, inevitable, and welcome.

— Michael Saylor (@saylor) July 18, 2026

The argument is that companies can move Bitcoin beyond a market driven primarily by individual ownership. Corporations can raise money, issue securities, access credit and maintain acquisition strategies at a scale that most individual buyers cannot reproduce.

That may help explain how Bitcoin’s market value can rise faster than conventional network indicators. One large corporate purchase can introduce more capital than thousands of small onchain users while creating far less visible activity.

It does not make the Metcalfe divergence irrelevant.

Corporate demand is more concentrated than broad user adoption and can depend on financing conditions, executive decisions, shareholder support and access to capital markets. A small number of large buyers can have a powerful effect while they are accumulating, but the market also becomes more sensitive to any slowdown in their purchases.

Saylor’s position is therefore a thesis rather than proof that the valuation gap has already been justified. Corporate adoption could provide the missing demand, but companies must continue allocating real capital for that explanation to hold.

Why Visser Thinks AI Changes the Bitcoin Comparison

In a recent discussion with Anthony Pompliano on The Pomp Podcast, Jordi Visser approached the same market from a different direction.

Visser is a veteran macro investor with more than 30 years of experience. His longer-term Bitcoin thesis is built partly around the effect artificial intelligence could have on public companies and traditional business models.

AI may increase productivity, but it can also weaken the competitive advantages on which corporate valuations depend. Software can be replicated, operating costs can collapse, products can become easier to reproduce and established industries can be reorganized by new competitors.

Bitcoin does not operate like a conventional company. It has no management team, profit margins or commercial business model for an AI competitor to disrupt.

For Visser, that makes Bitcoin the only asset whose competitive “moat” he does not have to worry about AI attacking.

The argument does not mean Bitcoin is protected from market risk. Its price can still fall because of leverage, liquidity, regulation, changing investor demand or broader risk reduction. Visser’s point is more specific: technological disruption that damages a company’s expected earnings does not attack Bitcoin through the same channel.

That distinction became more important during the recent unwinding of leveraged positions in AI-related stocks.

Using the volatility figures cited in the discussion, Visser said volatility in the broader AI thematic trade had moved toward 100, while Bitcoin volatility remained near 30. On a simple volatility-adjusted basis, that would theoretically allow a portfolio to hold roughly three times more Bitcoin exposure than AI exposure without increasing its measured volatility.

The comparison should not be treated as a portfolio recommendation. Volatility scaling does not fully account for sudden drawdowns, liquidity conditions, changing correlations or the possibility that historical relationships break during a market shock.

It nevertheless supports a broader observation. Bitcoin became comparatively easier to hold while another major speculative theme was being deleveraged.

That relative resilience could attract investors searching for a new source of market exposure after the sharp rise in AI-related volatility. Visser said he remained considerably more heavily weighted toward crypto than toward the semiconductor positions he had recently begun rebuilding.

His crypto exposure consisted of Bitcoin, Ethereum and shares in Strategy, formerly known as MicroStrategy.

Cooler Inflation Improves the Short-Term Backdrop

The immediate macro environment has also become less hostile.

The U.S. Consumer Price Index fell 0.4% in June, its largest monthly decline since April 2020. Energy prices fell 5.7% and were the largest contributor to the drop.

Headline inflation remained at 3.5% over the previous 12 months, while the index excluding food and energy was unchanged in June and increased 2.6% over the year.

Visser interpreted the report as evidence that inflation may become less important to financial markets during the remainder of the year. The softer reading also reduced expectations that the Federal Reserve would need to raise interest rates again, which he views as positive for crypto and the broader debasement trade.

That interpretation goes beyond what the official data alone can establish. One monthly decline does not guarantee that inflation has been defeated, particularly when much of the drop came from energy prices that can reverse quickly.

The Federal Reserve also remains more cautious. At its June meeting, the central bank maintained the federal funds target range at 3.5% to 3.75% and continued to describe inflation as elevated relative to its 2% goal.

Bitcoin’s relative stability during the recent momentum unwind was encouraging for Visser, but he acknowledged that crypto prices had not yet reflected the full potential benefit of falling rate-hike expectations.

That leaves the short-term case supportive but incomplete. Cooler inflation removes one source of pressure, but it does not automatically create the sustained buying needed to close the gap between Bitcoin’s valuation and visible network adoption.

The Fiscal Deficit Is the Longer-Term Anchor

The deeper foundation of Visser’s crypto position is not one inflation report or one Federal Reserve decision. It is the structural U.S. fiscal deficit.

The Congressional Budget Office projects a federal deficit of approximately $1.9 trillion in fiscal 2026, equal to 5.8% of gross domestic product.

Federal outlays are projected to reach 23.3% of GDP, compared with revenues equal to 17.5%. Debt held by the public is expected to reach 101% of GDP during the year and continue rising over the following decade.

That persistent gap is the basis of the debasement argument.

Large deficits do not produce an automatic or immediate increase in Bitcoin’s price. They do, however, require continued government borrowing and contribute to concerns about debt sustainability and the long-term purchasing power of government-issued currencies.

Bitcoin’s fixed supply allows investors to express those concerns through an asset outside the conventional monetary system.

Visser’s position is therefore not that each new deficit dollar flows directly into crypto. It is that persistent fiscal expansion creates a continuing reason for corporations, institutions and macro investors to seek assets whose supply cannot be increased in response to government financing needs.

That long-term argument also helps connect his view with Saylor’s.

Visser explains why investors may want a scarce monetary asset. Saylor explains how companies and financial structures could channel capital into it at scale.

Together, their arguments raise the question at the center of the current market: can corporate and institutional capital validate a Bitcoin price that has already moved ahead of visible onchain adoption?

Bitcoin Is Pricing In a Different Kind of Adoption

Metcalfe Ratio near 3.23

Saylor’s corporate thesis

Visser’s AI thesis

Inflation and fiscal conditions

Bitcoin’s price is effectively betting that adoption is changing shape.

The onchain data says valuation has moved ahead of the activity visible in Alphractal’s model. Saylor argues that companies can provide the capital, scale and continuity required to extend Bitcoin’s monetary network, while Visser explains why AI disruption and persistent fiscal deficits could give portfolios a reason to make that allocation.

The thesis remains conditional.

If corporate and institutional demand continues to expand, the gap between valuation and network activity may reflect adoption migrating into custodial products, corporate balance sheets and concentrated investment vehicles.

In that scenario, conventional onchain indicators would still describe an important part of the network, but they would capture only part of the capital supporting Bitcoin’s market value.

If those flows weaken while network activity remains subdued, the same divergence becomes harder to defend. Bitcoin would then rely increasingly on speculation and expectations of future demand rather than adoption already taking place.

The next test is therefore not only whether more people transact directly on Bitcoin. It is whether corporations, funds and macro investors can turn a less visible form of adoption into durable demand.

The price is already anticipating that transition. The capital now has to confirm it.

This article is provided for informational purposes only and does not constitute financial or investment advice.

Kosta has reported on cryptocurrency markets and blockchain infrastructure since 2020, bringing over six years of hands-on experience in the crypto industry built through daily tracking of markets, trends, and emerging blockchain developments. Specializing in Bitcoin on-chain analysis, institutional ETF flows, and digital asset price action, his work at Coindoo has been cited by other news agencies and consistently covers market developments with a focus on data-driven reporting across Bitcoin, Ethereum, Solana, and XRP. Over the years, Kosta has contributed to multiple crypto media outlets in different regions, authoring over 6,000 articles across the sector. His reporting spans cryptocurrency markets and the broader fintech industry, tracking not only price action but also the technological and regulatory forces shaping the ecosystem. To support his analysis, Kosta actively leverages on-chain data and metrics from leading platforms such as Santiment, Glassnode, and CryptoQuant, enabling deeper, evidence-based market insights. He believes in the power of transparency and the data that underpins the blockchain ecosystem. His academic background in Marketing Management from Denmark further complements his analytical approach, adding a strong understanding of communication strategy and content positioning to his work.