Polygon CPO On Why He Thinks Stablecoins Are Crypto’s Killer Use Case

Speaking at ETHCC, Polygon's Chief Product Officer John Egan argued that crypto's killer use case turned out to be moving money, specifically stablecoins as a payment rail, not NFTs, DeFi speculation, or trustless infrastructure as an end in itself. "The killer use case for crypto is money," he said.

Key Takeaways

- Polygon’s John Egan argues stablecoins are crypto’s real killer use case.

- Polygon processed $80 billion in stablecoin volume in May 2026.

- It holds over 75% of non-USD stablecoin activity globally.

- His AI-agent and on-chain-FX claims are projections, not current data.

The Thesis: Money Was Always the Endpoint

“The killer use case for crypto is money,” he said, framing it not as a pivot but as the natural destination the technology was building toward, the same way the internet’s killer use case turned out to be commerce rather than email. The parallel is worth sitting with, because it reframes a decade of crypto experimentation as a search that’s now resolved. “Our mission now is to move all money on chain,” Egan said, adding that money “should be productive, useful, easily accessible, global.”

It’s a clean thesis, and notably, the argument holds whether or not you accept Polygon’s particular role in it. The claim isn’t that one chain wins; it’s that stablecoin payments are the use case that finally found product-market fit.

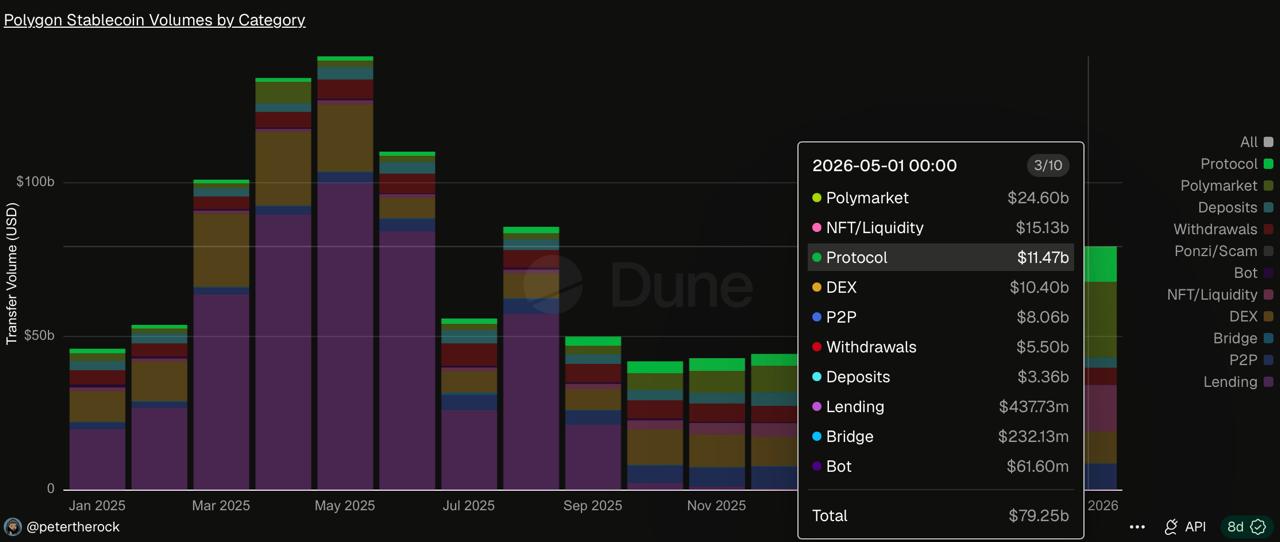

The Current Proof

The data Egan points to is concrete. According to Dune, Polygon processed $79 billion in stablecoin volume in May 2026, which, by his account, exceeded both Solana and BNB in transaction count and total volume that month.

The network also holds more than 75% of non-USD stablecoin activity globally. For throughput context, Polygon currently runs around 5,000 transactions per second, roughly in line with what traditional card networks like Visa and Mastercard process today, with an internal target of 100,000 TPS via its Giga Gas upgrade.

The most analytically useful proof point is geographic. Stablecoin volume in Brazil and Latin America, Egan argues, can’t be dismissed as wash trading, because the economic incentive to fake it isn’t there. People using stablecoins for daily transactions in markets with currency instability are real utility users by definition. That’s the cleanest rebuttal to the perennial “crypto volume is fake” critique: in economies where the local currency is unreliable, a dollar-pegged token doing everyday work is genuine demand, not manufactured activity.

The Non-USD Angle

The 75% non-USD figure points to where Egan thinks the next phase of stablecoin growth is happening. The USDT and USDC duopoly dominates dollar-denominated volume, but euro, yen, and local-currency stablecoins, serving users who want on-chain foreign-exchange access without routing through the dollar first, are growing on Polygon. Egan’s broader argument here is forward-looking rather than a current data point, and worth flagging as such: he sees on-chain FX eventually replacing the bank-style ramp, where the same provider that converts your money also sets your exchange rate with a hidden margin. That’s a structural prediction, not something the numbers yet confirm.

The Infrastructure Moment: Mastercard

One concrete sign that traditional finance is integrating these rails rather than resisting them is Mastercard’s announced agent-payment protocol, in which Polygon is a participant. The protocol targets two specific use cases: AI agent-to-agent payments, and direct merchant settlement in stablecoins outside normal banking hours, after hours, weekends, and holidays.

The significance is access. Mastercard brings an existing global merchant network, the kind of adoption infrastructure that blockchain payments couldn’t replicate on their own. That’s the meaningful part, and it’s worth keeping in proportion: it’s a participation in a protocol, not a wholesale migration of Mastercard’s business onto a blockchain.

The Forward Case: The Agent Economy

Egan’s most speculative argument is about AI agents, and it should be read as a projection, not a fact. “Agent transaction volume will exceed that of humans in five years,” he said. The mechanism he describes is genuinely interesting: agents spawning sub-agents, those sub-agents transacting with other sub-agents, each one immediately redeploying funds it receives, which requires instant, irreversible settlement. Credit networks built around reversibility don’t fit that model, because a payment that can be clawed back can’t be instantly redeployed with certainty.

That’s the structural case for why blockchain settlement specifically suits an agentic economy, and it’s a coherent one. But the five-year timeline and the scale of agent transactions are forecasts. The logic of why blockchains fit agent payments is sound; whether agent volume actually overtakes human volume on that schedule is unknowable today.

The Honest Counter

Two caveats keep this grounded. First, much of the bullish framing comes from a Polygon executive speaking at a crypto conference, so the competitive claims, that Polygon is already the dominant chain, or that rivals’ volume is largely wash trading, are his view and Polygon’s positioning, not settled fact. The $80 billion volume figure and the non-USD share are specific, checkable claims; the “we’re winning” framing around them is advocacy.

Second, the genuine open question is concentration. The stablecoin market today is dominated by the USDT and USDC duopoly, and whether the non-USD, multi-chain diversification Egan describes actually broadens that, or whether stablecoins stay concentrated in a few dollar-pegged giants, is genuinely uncertain. The core thesis, that money movement is crypto’s killer use case, looks increasingly hard to argue with. Which chains and which currencies capture it is the part still being decided.

Kosta has reported on cryptocurrency markets and blockchain infrastructure since 2020, bringing over six years of hands-on experience in the crypto industry built through daily tracking of markets, trends, and emerging blockchain developments. Specializing in Bitcoin on-chain analysis, institutional ETF flows, and digital asset price action, his work at Coindoo has been cited by other news agencies and consistently covers market developments with a focus on data-driven reporting across Bitcoin, Ethereum, Solana, and XRP. Over the years, Kosta has contributed to multiple crypto media outlets in different regions, authoring over 6,000 articles across the sector. His reporting spans cryptocurrency markets and the broader fintech industry, tracking not only price action but also the technological and regulatory forces shaping the ecosystem. To support his analysis, Kosta actively leverages on-chain data and metrics from leading platforms such as Santiment, Glassnode, and CryptoQuant, enabling deeper, evidence-based market insights. He believes in the power of transparency and the data that underpins the blockchain ecosystem. His academic background in Marketing Management from Denmark further complements his analytical approach, adding a strong understanding of communication strategy and content positioning to his work.