Stablecoins Could Change How European Banks Fund Loans

The European Central Bank is warning that stablecoins could become more than a competitor to cards and bank transfers. At sufficient scale, they could begin removing the retail deposits that European banks use to fund mortgages, business loans and other credit.

Key Takeaways

- ECB Executive Board member Piero Cipollone warned that wider stablecoin adoption could reduce the retail deposits funding European banks.

- Some of the money may return as issuer reserves, but in a more concentrated and less stable form.

- Roughly 99% of global stablecoin issuance is tied to the U.S. dollar, creating an additional monetary-sovereignty risk for Europe.

- The digital euro is being designed with no interest and holding limits to prevent it from becoming another destination for large deposit outflows.

Speaking in Rome on July 17, 2026, ECB Executive Board member Piero Cipollone drew a direct connection between the growth of private digital money and the funding available to commercial banks.

“If the use of stablecoins increases in the future, banks will also lose retail deposits,” Cipollone said in his official speech at the Federcasse Annual Meeting.

His warning was conditional. The ECB is not claiming that stablecoins have already caused a systemic deposit crisis in the euro area. It is arguing that their role would change if European households and businesses began using them routinely for savings, payments or corporate liquidity rather than mainly for crypto trading.

At that point, the issue would no longer be limited to competition between payment technologies. It would affect how banks finance themselves and how effectively ECB interest-rate decisions reach the wider economy.

A Stablecoin Purchase Changes Who Controls the Deposit

Money used to purchase a stablecoin does not necessarily disappear from the banking system. The more important change is where it ends up and how quickly it can leave again.

When a customer buys a stablecoin from a non-bank issuer, funds move out of the customer’s current or savings account. The issuer may then hold part of those funds as deposits at commercial banks and invest the remainder in short-term government securities or other permitted reserve assets.

Some of the original money therefore returns to banks, but not in its previous form.

A large number of relatively small household deposits is replaced by one or several corporate deposits controlled by a stablecoin issuer. Retail balances are usually considered a comparatively dependable funding source because they are spread across many customers and tend to move gradually. An issuer’s reserve deposit can be withdrawn rapidly and in large amounts when token holders demand redemption.

A March 2026 paper in the ECB Working Paper Series found that greater stablecoin adoption can shift funding from retail deposits toward wholesale sources. The researchers associated that transition with higher funding costs, greater dependence on market conditions and a possible reduction in lending to companies.

The effect is not automatic or equally strong at every level of adoption. The paper found negligible aggregate consequences while stablecoin use remained limited, with the impact rising as adoption became large enough to substitute meaningfully for bank deposits.

That distinction prevents two misleading conclusions. Stablecoins do not immediately remove every converted euro from the banking sector, but reserve deposits held by issuers are not economically equivalent to millions of separate household accounts.

MiCA Protects Redemptions but Cannot Recreate Retail Funding

Europe’s Markets in Crypto-Assets Regulation already imposes reserve, liquidity and redemption requirements on regulated stablecoin issuers.

Under the official MiCA text, at least 30% of the relevant reserves must generally be held as deposits with credit institutions. That requirement rises to at least 60% for significant tokens.

Those rules are intended to provide issuers with liquid assets and reduce the risk that redemption requests cannot be met. They also return part of the money collected from stablecoin buyers to the banking sector.

They do not, however, restore the original distribution of deposits.

Retail money leaving hundreds of thousands of customer accounts may return as concentrated corporate balances held at a limited number of banks. If confidence in the token deteriorates, the issuer may need to withdraw those reserves quickly to process redemptions.

The ECB has identified three related weaknesses:

MiCA therefore reduces some risks without turning stablecoin reserves into a perfect substitute for retail deposits. As the ECB explained in a June 2026 speech on stablecoins and money market funds, the same reserve rules can also increase the financial connection between token issuers and the banks holding their assets.

Stress can move in both directions. The failure of a reserve bank can threaten a stablecoin’s peg, while mass stablecoin redemptions can remove substantial deposits from partner banks.

Cross-border issuance creates another complication. When fungible versions of the same token are issued by related entities inside and outside the EU, MiCA protections cover the European issuer but not necessarily the foreign entity.

During a run, holders may prefer to redeem through the EU entity because European rules provide stronger redemption safeguards. The reserves ring-fenced in Europe may not be large enough to satisfy demand generated across the entire global token supply. The ECB has called for stronger safeguards before such multi-issuer arrangements are allowed to operate at scale.

Stablecoin holders also do not receive the same protection as bank depositors. Central-bank emergency liquidity is designed for qualifying solvent banks, not private token issuers, while stablecoin balances are not covered as ordinary deposits under traditional deposit-guarantee schemes.

Dollar Stablecoins Add a Monetary-Sovereignty Risk

The source of the deposit is only one part of the ECB’s concern. The currency attached to the token also matters.

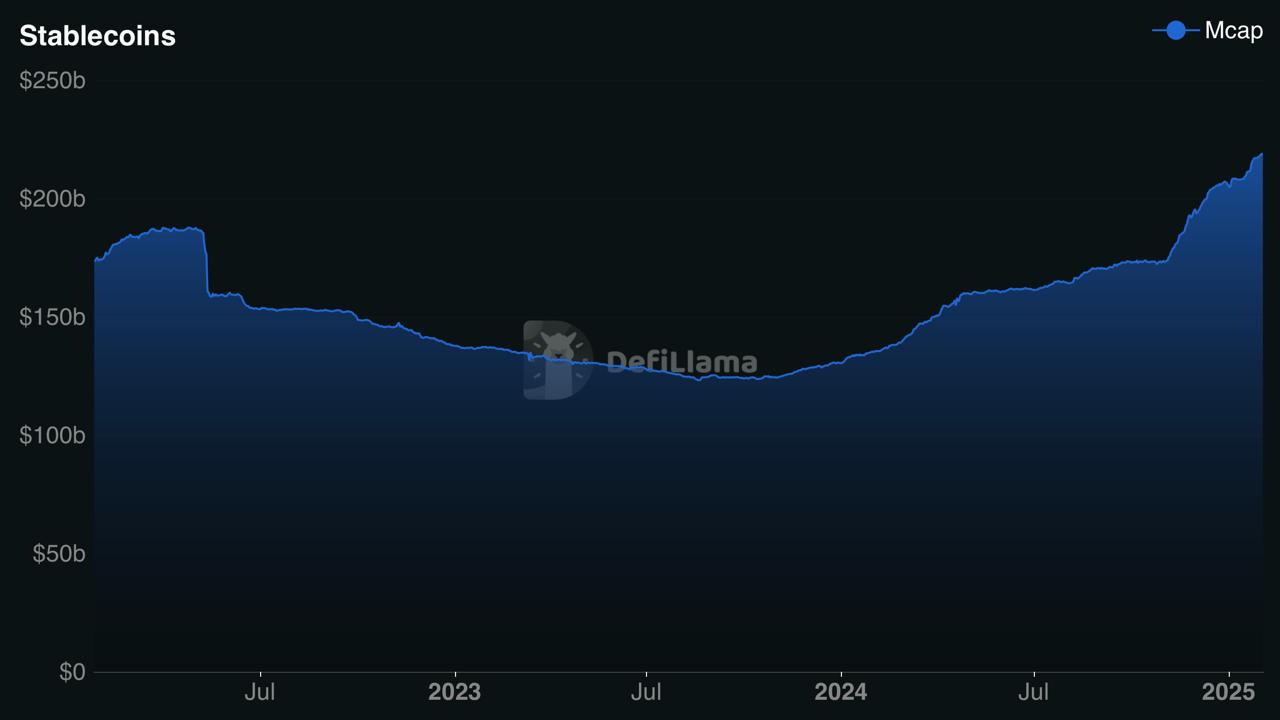

Approximately 99% of global stablecoin issuance is denominated in U.S. dollars, according to ECB research. The figure refers to the share of stablecoin supply rather than exactly 99% of all transaction volume.

Tether’s USDT and Circle’s USDC dominate the market by a wide margin. Defillama data show USDT with a market capitalization of approximately $184 billion and USDC with $73.4 billion. Together, the two dollar-pegged tokens account for roughly $257.4 billion, or about 83% of the total $310 billion stablecoin market. Euro-denominated stablecoins remain only a small fraction of the sector, leaving most global stablecoin liquidity tied to the U.S. dollar.

Widespread use of dollar tokens by European households and businesses could introduce foreign monetary conditions into the euro-area economy. Demand for liquidity might begin responding more strongly to U.S. interest rates, dollar funding conditions and confidence in foreign issuers, even when those developments do not match the ECB’s domestic policy stance.

The March ECB research paper describes how this could weaken monetary-policy transmission. Banks relying more heavily on foreign-currency wholesale funding may respond less predictably to changes in ECB rates, reducing the central bank’s influence over local lending conditions.

The risk goes beyond which currency appears on a digital wallet. If European tokenized markets and cross-border payments settle mainly through dollar stablecoins, an increasing share of the region’s financial infrastructure would depend on private issuers and payment rails governed outside Europe.

Stablecoins may still offer faster settlement, continuous availability and lower friction for some transactions. The ECB’s argument is that those operational benefits do not remove the consequences of allowing foreign private money to become a major store of liquidity inside the euro area.

The Digital Euro Is Designed Not to Become a Savings Account

Cipollone presented the digital euro as the ECB’s answer to two related problems: Europe’s dependence on foreign payment providers and the risk that new forms of digital money marginalize commercial banks.

The proposed system would not bypass banks. Commercial lenders and other authorized payment providers would distribute digital euros, open customer accounts and handle the relationship with users. Banks would retain access to transaction records needed for compliance, credit assessment and risk management.

The design also includes mechanisms intended to stop the digital euro from pulling large amounts of money out of bank accounts:

No interest would be paid on digital euro holdings;

Individual holding limits would restrict how much could be stored;

Links to current accounts would allow payments above the available digital euro balance without requiring users to hold large amounts in advance.

The exact holding limit has not yet been finalized. The ECB says it will be calibrated to preserve usability without harming bank liquidity, financial stability or monetary-policy transmission.

That creates a structural difference from private stablecoins. MiCA prohibits issuers and crypto service providers from paying interest on regulated stablecoin holdings, but it does not impose the same type of universal individual holding cap envisioned for the digital euro.

The digital euro is therefore being built primarily as a payment instrument, not as an unlimited savings vehicle.

Technical preparations are moving ahead. On July 14, the ECB selected 36 payment service providers for a 12-month pilot scheduled to begin in September 2027.

The participants include Deutsche Bank, Revolut Bank, Adyen, Stripe, UniCredit, Worldline and other bank and non-bank providers from across the euro area. They will test a beta version through person-to-person, in-store, e-commerce and offline payment scenarios involving Eurosystem staff and selected merchants.

The pilot currency will not have legal-tender status. Its purpose is to test the infrastructure, operating processes and user experience before any final issuance decision.

The ECB aims to be ready for a potential first issuance in 2029, assuming the required EU legislation is completed in 2026. That date is not a guaranteed public rollout: the final decision to issue a digital euro can only come after the legal framework is adopted.

Cipollone’s warning ultimately concerns scale rather than the existence of stablecoins. At their current euro-area footprint, they are not dismantling the commercial banking system. If they become a widely used destination for household and corporate liquidity, however, their effect would extend from crypto markets into bank funding, credit availability and monetary policy.

The decisive indicators could be whether stablecoin use moves beyond trading, where issuer reserves are deposited, how concentrated those balances become and whether dollar tokens gain a meaningful role in everyday European payments.

The information provided in this article is for educational purposes only and does not constitute financial, investment, or trading advice.

Kosta has reported on cryptocurrency markets and blockchain infrastructure since 2020, bringing over six years of hands-on experience in the crypto industry built through daily tracking of markets, trends, and emerging blockchain developments. Specializing in Bitcoin on-chain analysis, institutional ETF flows, and digital asset price action, his work at Coindoo has been cited by other news agencies and consistently covers market developments with a focus on data-driven reporting across Bitcoin, Ethereum, Solana, and XRP. Over the years, Kosta has contributed to multiple crypto media outlets in different regions, authoring over 6,000 articles across the sector. His reporting spans cryptocurrency markets and the broader fintech industry, tracking not only price action but also the technological and regulatory forces shaping the ecosystem. To support his analysis, Kosta actively leverages on-chain data and metrics from leading platforms such as Santiment, Glassnode, and CryptoQuant, enabling deeper, evidence-based market insights. He believes in the power of transparency and the data that underpins the blockchain ecosystem. His academic background in Marketing Management from Denmark further complements his analytical approach, adding a strong understanding of communication strategy and content positioning to his work.