IMF Identifies Stablecoins as Tokenization’s Weakest Link: Here is Why

IMF's note on tokenized finance warns that stablecoins resemble money market funds, not central bank money. The data suggests the stakes of getting this wrong have never been higher.

Key Takeaways

- IMF classifies tokenization as a structural shift in financial architecture.

- Stablecoins described as resembling money market funds.

- Monthly stablecoin transaction volume exceeded $1.8 trillion.

- Emerging economies face sharpest exposure .

The International Monetary Fund published comprehensive note on tokenized finance in April 2026, authored by Tobias Adrian, the Fund’s Financial Counsellor. The document is not a general overview. It is a policy argument, and its central claim is unambiguous: tokenization does not improve the existing financial system. It replaces the architecture through which trust, settlement, and risk management are organized.

Previous waves of digitization, electronic payments, online trading, algorithmic execution, worked within existing institutional boundaries. Banks remained banks. Custodians remained custodians. Settlement remained sequential. Tokenization reconfigures those boundaries themselves. When ownership, transfer, and compliance are embedded directly into programmable tokens on shared ledgers, the locus of risk shifts from institutions to infrastructure. Failures no longer originate in balance sheets. They originate in code.

That shift is where the crypto-specific implications begin, because stablecoins are the settlement layer on which tokenized crypto markets already operate. And the scale of that settlement layer is now impossible to dismiss.

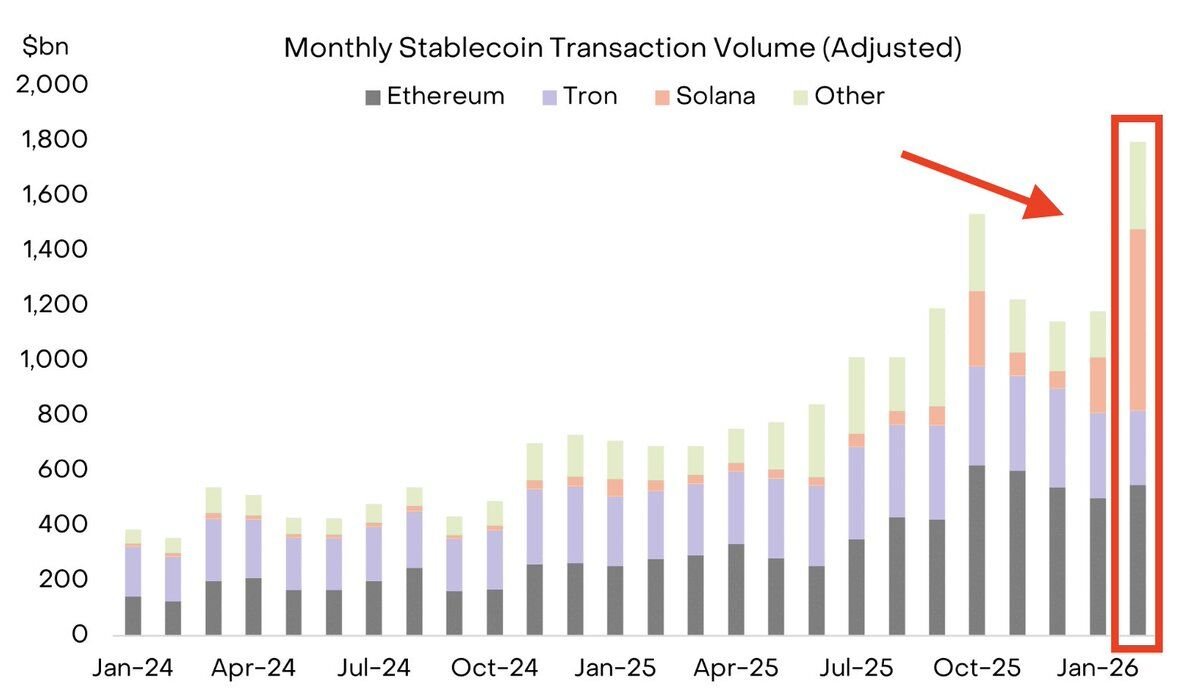

$1.8 Trillion a Month – What the Chart Shows

Stablecoin transaction volume hit $1.8 trillion per month by early 2026 according to our recent report on stablecoins, a number that, placed against the near-zero baseline of 2018, represents one of the most compressed expansions in modern financial history.

From 2018 through 2020, monthly volumes were negligible, tens of billions, barely registering on the scale. Through 2021 and 2022, volume climbed into the 300–400 billion range as stablecoins became the primary settlement instrument within crypto markets. The acceleration that followed was not gradual. From 2024 onward, successive thresholds, 600 billion, 800 billion, 1.2 trillion, were broken in sequence until the early 2026 figure marked a near-vertical departure from everything that preceded it.

What that chart is showing is not speculative demand. It is settlement activity. According to the report, stablecoins are evolving into the monetary foundation of the emerging token economy, influencing money markets, payment systems, and treasury structures simultaneously. With 97% of all stablecoins denominated in U.S. dollars, their growth is also a geopolitical event. While Europe is focusing on control and stability through MiCAR regulation, the United States is increasingly positioning dollar-based stablecoins as a strategic instrument, effectively extending dollar dominance into the tokenized economy without a formal policy decision to do so.

The IMF is not warning about a niche instrument. It is warning about $1.8 trillion in monthly settlement activity built on infrastructure it describes as the weakest link in the tokenized financial system.

The Stablecoin Problem

The IMF identifies three categories of tokenized money: tokenized deposits, regulated stablecoins, and wholesale CBDCs, each carrying a different allocation of risk. The Fund is clearest about where the weakest point lies.

Stablecoins resemble money market funds more than central bank money. A fully backed stablecoin can still break its peg, not because reserves are insufficient, but because the market through which those reserves must be liquidated seizes up exactly when redemption demand spikes. This is not theoretical. It is the same mechanism that caused money market funds to break the buck in 2008.

The IMF does not call for banning stablecoins. It calls for clarity about what they are, pointing to a synthetic CBDC model, where private issuers fully back tokens with central bank reserves, as the arrangement that preserves innovation while anchoring settlement in public trust. The distinction matters because as stablecoins move from crypto trading rails toward settlement assets in tokenized capital markets, the systemic consequences of a run grow proportionally with the $1.8 trillion monthly volume they already carry.

This is precisely why the IMF singles out stablecoins as the weakest link in tokenization specifically. Every other component can theoretically fail and be contained, a smart contract can be paused, a ledger can be forked, a CCP wound down. Stablecoins cannot be contained the same way because they are the settlement layer through which every other component connects. When the money that settles everything else breaks its peg, it fails simultaneously across every tokenized transaction, every collateral position, and every liquidity pool that relied on it. The IMF’s warning is not that stablecoins are the most fragile component. It is that they are the most consequential one to break.

The Speed Problem

In traditional finance, settlement lags exist not only because of inefficiency. A transaction that takes two days to settle is a transaction that can be unwound, netted, or paused if something goes wrong. Those two days are the window in which a regulator can intervene, a counterparty can raise collateral, and a liquidity crisis can be identified before it becomes a solvency crisis. Atomic settlement closes that window permanently.

In a tokenized system, a faulty price feed or a coding error can trigger cascading liquidations across interconnected smart contracts before a regulator has identified the problem. The IMF is explicit: stress events in tokenized markets will unfold faster than in traditional systems, leaving less time for discretionary intervention. Automated margin calls triggered by price movements can force rapid asset sales at exactly the moments when markets are least able to absorb them, amplifying volatility rather than damping it.

Central bank backstops designed around business-day cycles are structurally inadequate in a 24/7 automated environment, and stablecoins, operating as the settlement layer of that environment, are the first instrument that would be tested if the system came under stress.

The Fragmentation Risk and Why Emerging Economies Bear It First

The most alarming observation in the report concerns not the mature financial system but the developing one. Dollar-denominated stablecoins can now move across borders at machine speed, outside regulated banking channels. In an economy experiencing currency pressure, a central bank that might previously have had days to respond to capital outflows now faces a system where reserves can be depleted before an intervention order is executed. The IMF frames this explicitly as a sovereignty risk, not a market risk, because the tools that traditionally defend monetary sovereignty operate on timescales that tokenized capital flows have already made obsolete.

At the broader market level, the ecosystem is developing across multiple platforms without common interoperability standards. Liquidity fragments across those platforms. Cross-ledger bridges introduce new vulnerabilities. The IMF’s assessment is direct: fragmentation can be as dangerous as concentration, and the current trajectory is toward fragmentation.

The Contradiction and What the Data Actually Concludes

Taken together, the IMF report and the transaction data point to a conclusion that is genuinely uncomfortable: stablecoins are simultaneously the stability mechanism that makes crypto markets function and the systemic vulnerability that the IMF has formally identified as requiring urgent policy attention.

Within the crypto ecosystem, stablecoins are essential infrastructure. They give traders a way to exit volatile positions without leaving the blockchain, provide a 24/7 settlement currency across DeFi lending and liquidity pools, and function as the dollar of the token economy. Without them, the crypto market as it currently exists does not work. That is not a minor observation, it is the reason the IMF’s warning carries weight rather than dismissal.

The IMF’s “weakest link” characterization is not a moral judgment. It is a structural one. In any chain, the weakest link is not the smallest component, it is the one whose failure breaks everything else. Stablecoins occupy that position because they sit at the intersection of every other component in the tokenized architecture.

Smart contracts settle in them. Collateral positions are denominated in them. Liquidity pools depend on them. When every other part of a tokenized system uses stablecoins as its settlement currency, a loss of confidence is not a contained event. It is a system-wide event, arriving at machine speed, with no central bank standing behind it. A smart contract can be paused. A shared ledger can be forked. A stablecoin that has broken its peg cannot be recalled.

The optimistic case is that the infrastructure for a safer version already exists. Project Jura, Project Agorá, and the DTCC’s tokenized collateral pilot all demonstrate that atomic settlement in central bank money is technically achievable. Policy problems, unlike technical ones, have a history of getting solved when the stakes become visible enough.

The pessimistic case is that at $1.8 trillion in monthly volume, the stakes are already visible, and the legal certainty, cross-border resolution frameworks, and interoperability standards the IMF calls for do not yet exist in any jurisdiction.

The IMF’s roadmap is a construction manual for a safer architecture. The recent data shows how fast the current architecture is scaling. The gap between those two timelines is where the risk lives.

The information provided in this article is for educational purposes only and does not constitute financial, investment, or trading advice. Coindoo.com does not endorse or recommend any specific investment strategy or cryptocurrency. Always conduct your own research and consult with a licensed financial advisor before making any investment decisions.

Alexander Zdravkov is a person who always looks for the logic behind things. He has more than 3 years of experience in the crypto space, where he skillfully identifies new trends in the world of digital currencies. Whether providing in-depth analysis or daily reports on all topics, his deep understanding and enthusiasm for what he does make him a valuable member of the team.