Stablecoins Will Run Global Payments, Stanley Druckenmiller Says as Regulations Catch Up

Renowned investor and billionaire Stanley Druckenmiller has spent years dismissing crypto. He makes one exception: stablecoins.

- Stanley Druckenmiller predicts stablecoins will power the global payment system within 10–15 years

- Stablecoins processed over $27 trillion in 2024 – more than Visa and Mastercard combined

- The GENIUS Act (signed July 2025) gave stablecoins their first federal regulatory framework in the U.S.

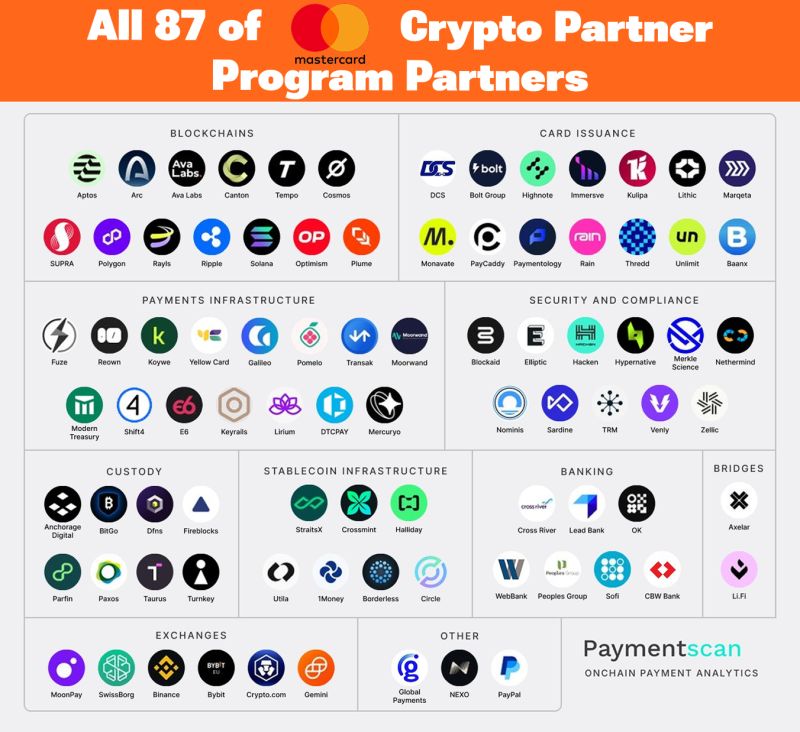

- Mastercard’s 87-partner crypto program signals institutional infrastructure is quietly being rebuilt from the ground up

In a Morgan Stanley interview released in March 2026, Druckenmiller stated that fiat-pegged digital tokens – primarily USDT and USDC – will serve as the backbone of the global payment system within the next 10 to 15 years. His reasoning isn’t ideological. It’s operational. Stablecoins, he argues, are faster, cheaper, and more efficient than the legacy financial infrastructure the world currently runs on.

“Incredibly useful” was the phrase he used. For Druckenmiller, that’s practically a standing ovation.

Where He Draws the Line

Don’t mistake this for a broader endorsement of crypto. Druckenmiller remains skeptical of the asset class at large, calling most cryptocurrencies “solutions looking for a problem” – a problem, he notes, that was never actually there to begin with.

Bitcoin gets a narrow carve-out. Not because he believes in its original pitch as a decentralized currency, but because the market has made up its mind. Bitcoin has built a brand, he concedes, and established itself as a credible store of value. That’s a concession, not a conviction.

His longer view is more provocative. Druckenmiller doubts the U.S. Dollar retains its reserve currency status in 50 years. His theory on what replaces it? Some form of digital asset – possibly a “crypto thing” he currently dislikes. He didn’t elaborate. He didn’t need to.

The broader investment context backs his read. The stablecoin market surpassed $300 billion in capitalization by 2025. Transaction volume in 2024 crossed $27 trillion – outpacing Visa and Mastercard combined. Investment bank Macquarie has described stablecoins as moving beyond niche trading instruments into a foundational layer of global financial infrastructure. Analysts at several firms are projecting 30–40% adoption in general payments within the next two years, with integration into platforms like Amazon and Google increasingly discussed as near-term probabilities.

The GENIUS Act: Washington Catches Up

The legislative machinery has started moving. The Guiding and Establishing National Innovation for U.S. Stablecoins Act – the GENIUS Act – was signed into law on July 18, 2025. It is the first federal regulatory framework for payment stablecoins in the United States, and its implications are significant.

The Act carves out a defined category of “Permitted Payment Stablecoin Issuers.” Banks can issue stablecoins through approved subsidiaries. Nonbank entities can apply for a federal license through the Office of the Comptroller of the Currency. Smaller state-level issuers – those with under $10 billion outstanding – can operate under state regimes, provided those regimes meet federal standards. Cross that threshold, and they move under federal oversight within 360 days.

Reserve requirements are strict. Every stablecoin must be backed 1:1 by high-quality liquid assets: U.S. dollars, Federal Reserve balances, demand deposits, or short-term Treasury bills. Rehypothecation – lending out or reusing reserve assets – is prohibited. Monthly public reports on reserve composition are mandatory. Issuers above $50 billion in circulation must produce annual audited financials.

READ MORE:

Solana Hits $650 Billion in Monthly Stablecoin Transactions as Grayscale Outlines 2026 Outlook

Consumer protections are built in. Holders can redeem at par value within two business days under proposed OCC rules. In the event of issuer insolvency, stablecoin holders take priority over all other creditors. Issuers cannot market their tokens as government-backed or FDIC-insured.

There’s one notable prohibition that generated significant debate: no interest or yield payments to holders. Regulators have flagged affiliate workarounds as likely violations. Big Tech companies not predominantly engaged in financial activities are also barred from issuing stablecoins without a unanimous federal waiver – a clause that appears aimed squarely at firms like Meta or Apple.

The Act also resolved a long-running legal ambiguity. Compliant payment stablecoins are explicitly not securities under SEC law and not commodities under CFTC law. Jurisdiction moves to banking regulators. That single clarification removed a major blocker for institutional adoption.

The regulatory clarity accelerated exactly what Druckenmiller predicted. Western Union and MoneyGram have already moved to integrate stablecoin infrastructure into their platforms.

Mastercard’s 87-Partner Blueprint

While the policy debate played out in Washington, the corporate infrastructure was being assembled quietly elsewhere. Mastercard’s Crypto Partner Program – now at 87 companies – isn’t a marketing initiative. It reads more like a financial system rebuild.

The partners span every layer of a modern payment stack. Blockchain rails: Solana, Polygon, Cosmos. Custody: Fireblocks, BitGo, Anchorage Digital. Stablecoin infrastructure: Circle, Crossmint, StraitX. Exchanges: Binance, Gemini, Crypto.com. Security and compliance: Elliptic, Hacken, TRM. Banking: Cross River, WebBank, Sofi.

The strategy isn’t replacement. Consumers will still tap cards. Merchants will still use payment service providers. But the settlement layer underneath – the part that moves money between institutions, across borders, in real time – is being quietly upgraded. Blockchain and stablecoins handle the back end. The front end stays familiar.

That’s a subtle but important distinction. The consumer experience doesn’t need to change for the financial infrastructure to shift fundamentally.

What Comes Next

The pieces are in place. Regulatory clarity exists. Institutional infrastructure is live. Macro credibility – via figures like Druckenmiller – is no longer in short supply.

The remaining question isn’t whether stablecoins become mainstream financial infrastructure. It’s how fast, under whose terms, and with what geopolitical consequences. Stablecoin corridors operating outside Western-controlled rails – involving jurisdictions like China, Russia, or Iran – are already being discussed in strategic policy circles as a genuine challenge to dollar dominance.

Druckenmiller’s 10–15 year timeline may be conservative. The architecture is already built. What’s left is adoption at scale – and that tends to happen faster than anyone’s forecast.

The information provided in this article is for educational purposes only and does not constitute financial, investment, or trading advice. Coindoo.com does not endorse or recommend any specific investment strategy or cryptocurrency. Always conduct your own research and consult with a licensed financial advisor before making any investment decisions.

Alexander Zdravkov is a person who always looks for the logic behind things. He has more than 3 years of experience in the crypto space, where he skillfully identifies new trends in the world of digital currencies. Whether providing in-depth analysis or daily reports on all topics, his deep understanding and enthusiasm for what he does make him a valuable member of the team.